The AI Future of B2B Software

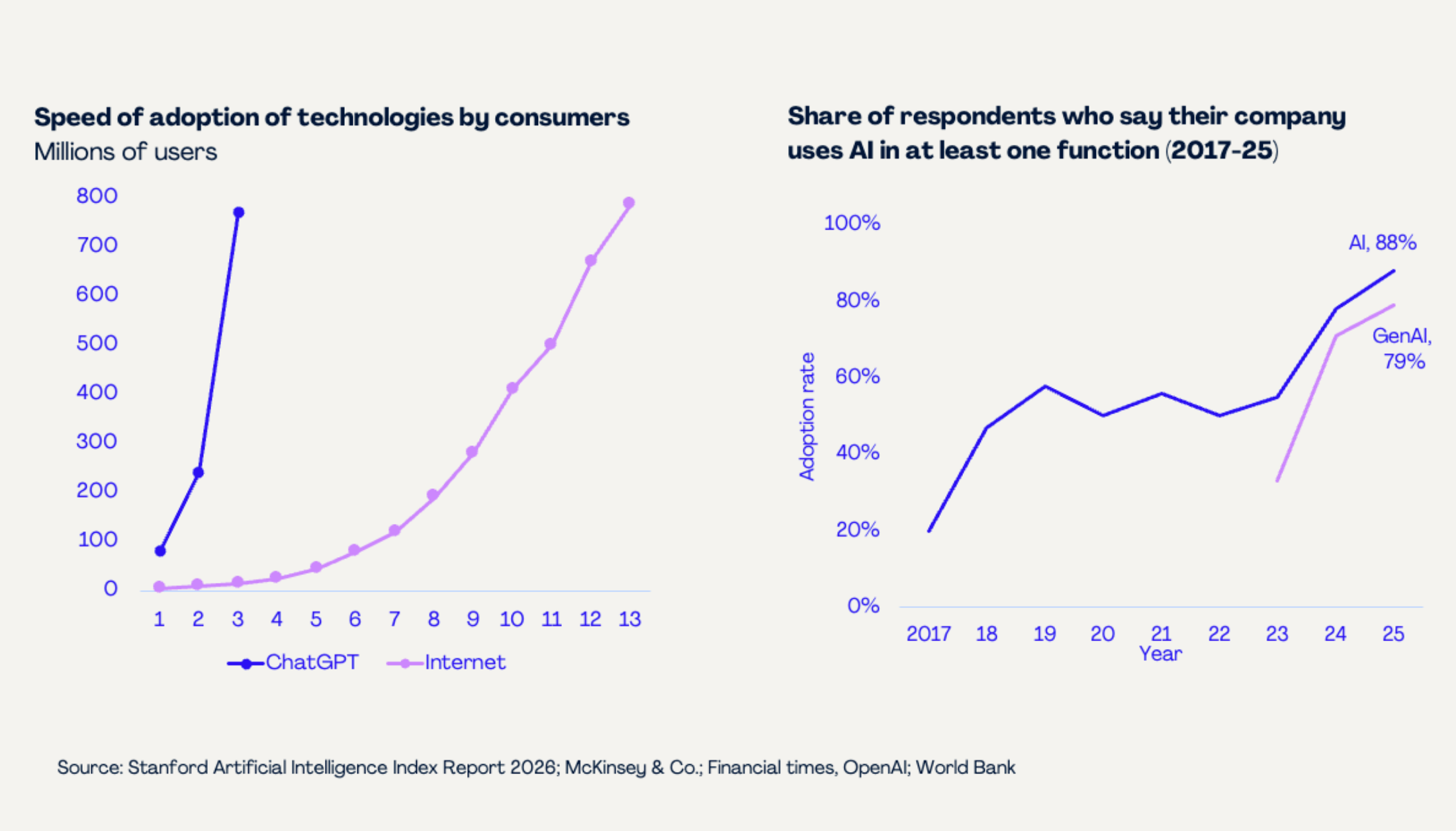

It has been four years since ChatGPT's public release, and the AI platform shift is outpacing even the internet's adoption. At Nauta, we believe we can now see the early shape of what this means for B2B software.

AI will grow the software market

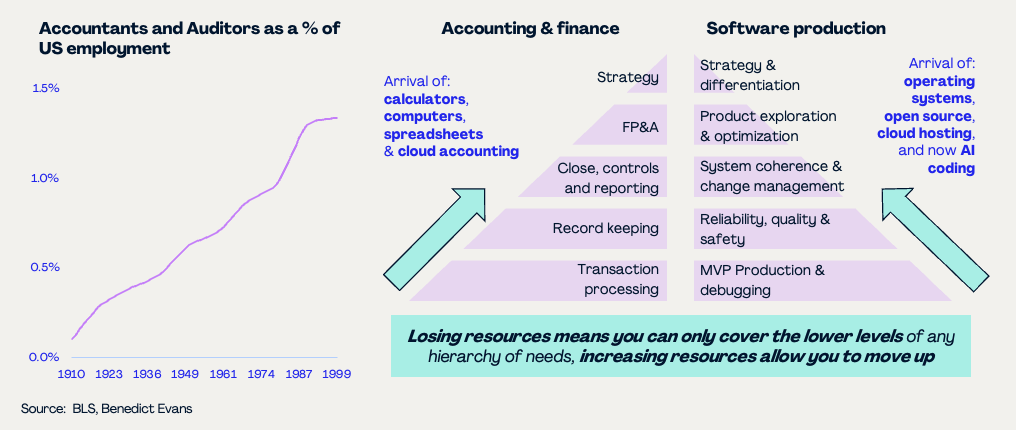

Software development is a textbook case of Jevon's paradox: as production costs fall, total spend rises. Calculators, computers and spreadsheets grew the accountancy market rather than shrinking it, because cheaper tools unlocked demand for higher-order work. The same pattern has played out across software's history with open-source software and cloud computing commoditising low-level work to help produce today's software giants. We believe that AI coding tools will do the same and further expand the market.

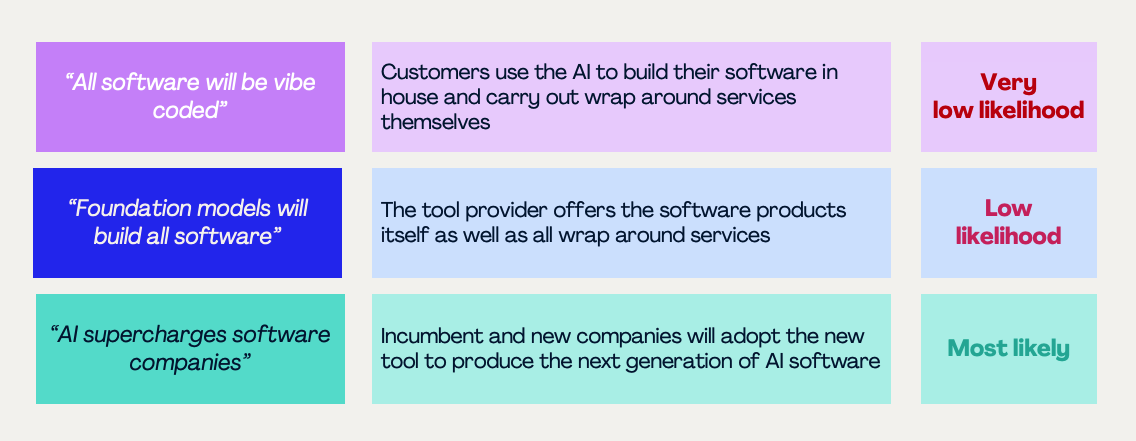

Tech companies building products with AI will have far more impact than clients "vibe-coding" in-house tools

Some commentators expect "vibe-coding" to produce a wave of in-house custom software. We disagree. Building software still requires judgement, taste and product decisions that are rarely a good use of time or resources for end clients. The primary output of AI coding tools will be externally built, managed and hosted software from tech companies that do the higher-order work beyond just writing code.

Vibe-coded tools and Claude automations are the new spreadsheets

The hidden cost of building software goes well beyond writing the code. Extensive testing, reliability engineering and ongoing maintenance are rarely factored in. There are also two errors people make when comparing an in-house vibe-coded tool to an off-the-shelf product: they are comparing an MVP to a production-grade system, and they are comparing it to yesterday's software, which is rapidly being commoditised. Economics almost always favours the off-the-shelf provider who spreads cost across many clients.

The new generation of software companies are building products far more capable than was previously possible. The brittle tools clients build in-house will look as dated as the messy spreadsheets the previous generation of software replaced.

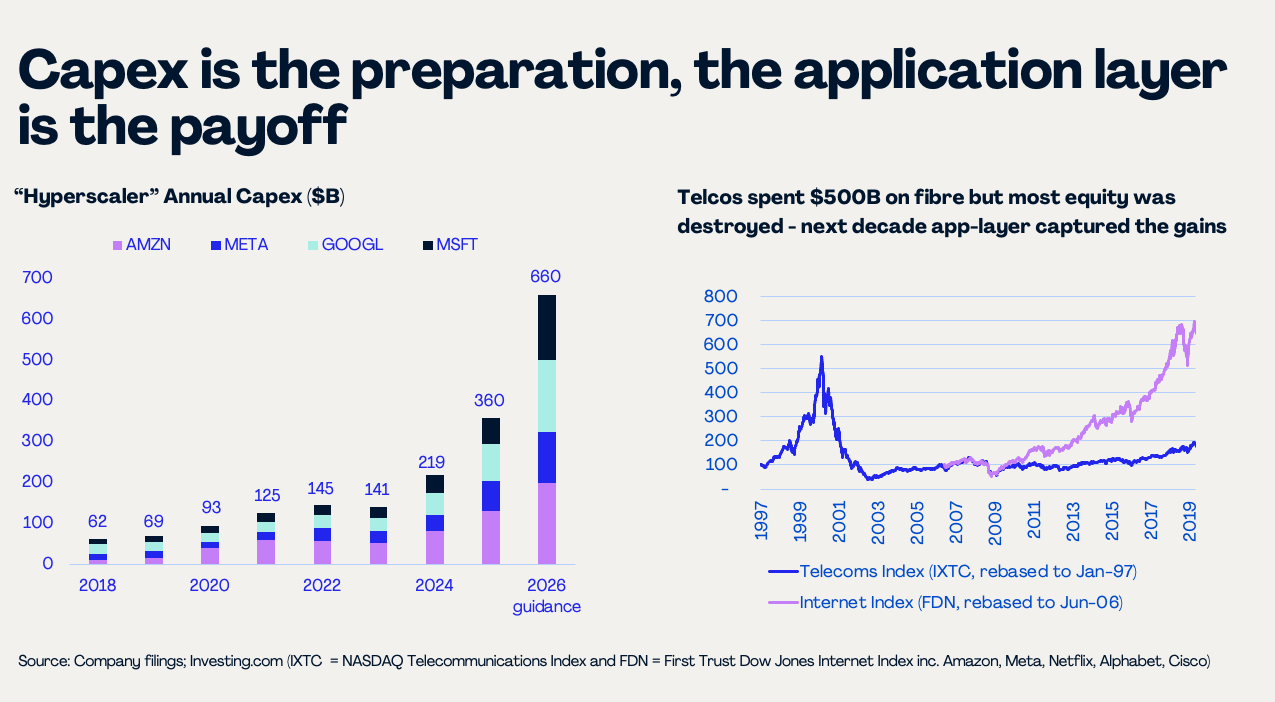

The application layer will capture most of the value from the platform shift

General-purpose model providers will build enormously valuable tools, but most enterprise workflows are highly specific. Application-layer products, vertical or horizontal, that leverage AI models within a purpose-built structure will serve these workflows and capture most of the value. The massive CAPEX investments being made today for training frontier models is simultaneously laying the groundwork for the next generation’s AI application layer.

AI will create a plethora of new software categories

The investment opportunities that excite us at Nauta are companies building products whose functionality and business model are centred around novel AI capabilities, often replicating increasingly commoditised incumbents along the way. Companies like Granola, Harvey/Legora and Fin are already building whole new categories and enabling workflows that simply were not possible before.

We look for investments where either no true incumbent exists, or where the adaptation required to compete with a new entrant would be deeply uncomfortable for the incumbent: workflows, data structures, tech stacks, product teams or pricing models that are no longer fit for purpose and must be rebuilt from scratch.

Software vendors will evolve towards model-performance-as-a-service

Historically, software vendors hosted, maintained and updated code and infrastructure. In the AI era, that is no longer enough. Vendors must also tune models, manage inference costs, monitor performance, build evaluation sets, ensure safety, maintain guardrails, handle hallucination risk and comply with AI governance requirements. These are complex, costly and highly domain-specific. The arena in which companies compete will evolve - away from product functionality, security and uptime and towards model performance.

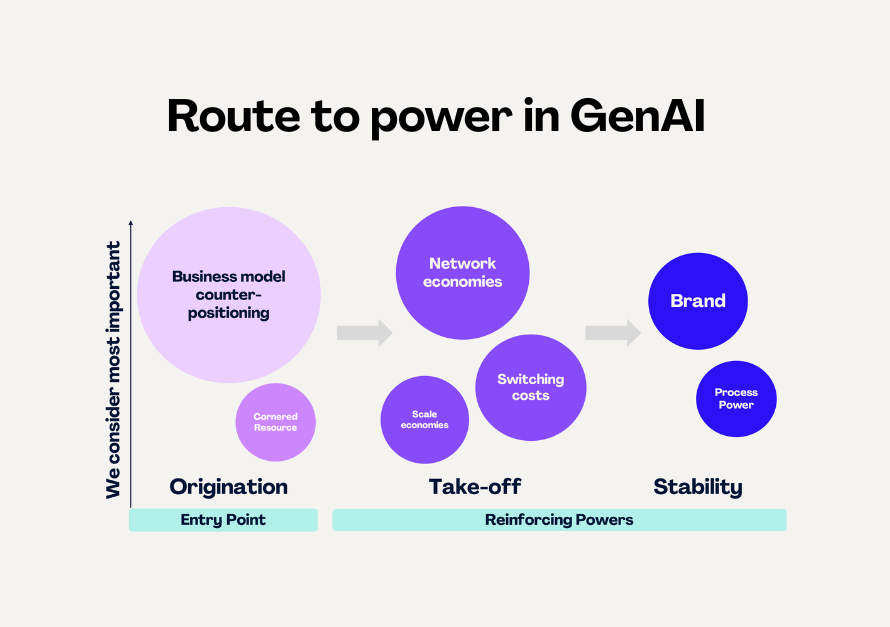

Model performance becomes the new arena for pricing power and defensibility

AI coding tools are eroding the differentiation that product functionality once provided. Model performance becomes both a costly investment and the primary opportunity to stand apart. Taking Fin as an example: clients choose it on price and resolution performance, and its defensibility compounds across counter-positioning against legacy support operations, switching costs from lost context, scale economies in training and testing, network effects from feedback data, and brand trust.

At Nauta, we assess companies on how they build defensibility that compounds over time, not just on the novelty of a capability that could easily be replicated.