Momentum vs. Moats: Building Durable GenAI Companies

Nowadays, the most common discussion in the tech ecosystem seems to be 'are we in an AI bubble?' Even Sam Altman and Mark Zuckerberg have acknowledged that we might be. But as Azeem Azhar (of research group Exponential View) reminds us, that’s not a very helpful question for right now: “bubbles are impossible to diagnose in real time. Only in retrospect do we know whether exuberance was justified or delusional.”

For us at Nauta, a more interesting question is ‘which GenAI companies will endure?’ Nauta has been investing in European B2B software for 20 years and through several cycles. We have seen drastic changes in consumer and investment appetite throughout, caused by technology paradigm shifts and macro-economic events, that propelled or bankrupted many companies and investors. So, to last as investors, we focus on founders whose vision will stand the test of time.

The fundamentals haven’t changed

Despite the claim that “everything has changed” thanks to AI, the fundamentals for a business at the application layer remain the same and the core questions still apply:

- Do customers love the product?

- Are they willing to pay for it?

- Do the unit economics work at scale?

What has changed is the speed of development, both at the infrastructure layer and for the applications built on top. This is where defensibility comes into question. Many now claim that moats are obsolete because application layer products can be easily replicated, and speed of execution is all that matters.

We disagree.

Firstly, it's unrealistic to think that GenAI can entirely replicate complex software products. While GenAI coding is dropping development costs, thus making scale economies - i.e., the advantage in marginal costs a big company gains by spreading its costs over millions of users or clients - less powerful, they won't disappear. The cost of a product goes beyond coding and testing; it requires investments in areas like regulatory compliance and commercial partnerships. Developing and maintaining a complete, enterprise-grade, secure product for near-zero cost remains an unlikely prospect.

More importantly, the idea that execution is the ONLY thing that matters today is also misguided. When there’s a huge global shift, whether political, economic or technological, the rules of the “game” change suddenly and often in a way that fundamentally undermines many legacy businesses. Under these circumstances, the importance of flawless execution rises significantly, favouring players that can move and adapt quickly and effectively.

However, while execution - especially in taste, velocity, and distribution - is critical and can even provide enough of an advantage for one player to outcompete another in the early days, it’s rarely sufficient to withstand competitive pressure in the long term. Instead, the factors that determine differentiation beyond the ‘sea change’ moment and pursuant land-grab will still be the same handful of factors as before. Moreover, most of these factors are ingrained in the very nature of the company’s business model, and pre-determined from early in the company’s life.

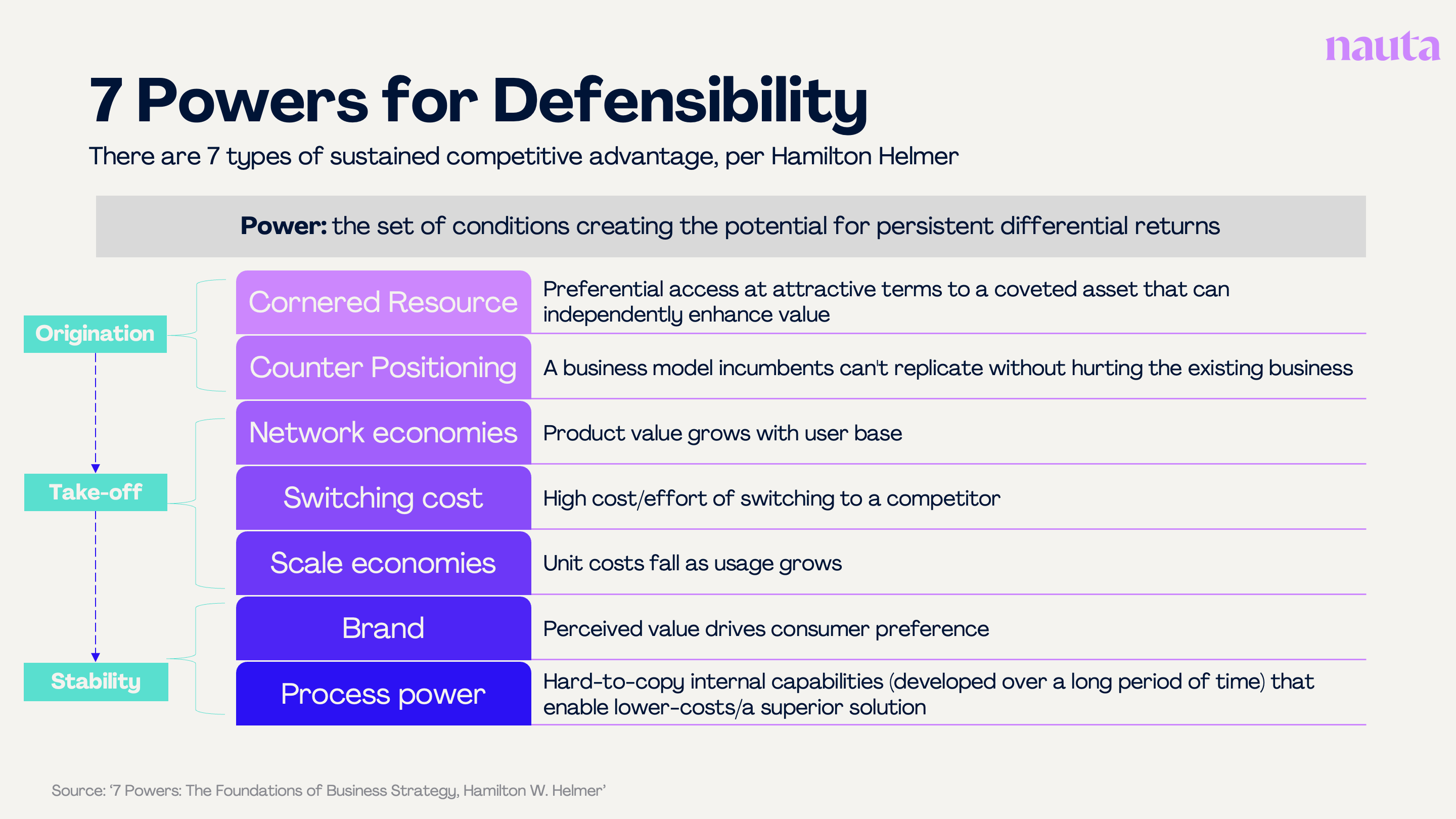

7 Powers still apply

In our view, Hamilton Helmer’s ‘Seven Powers’ are no less relevant in the GenAI era for long-term profit margin superiority, they just seem less important in the short term because executional ability steals more attention immediately after a transformational development. The Helmer Powers (referred to from this point onwards as “Powers”) allow a company to earn persistent differential returns versus competitors by allowing it to charge higher prices or realise lower costs and are a logical inevitability of competitive industries.

These Powers are key to generating business value at any time in history, even if the prevalence of a given Power may change from one economic cycle to the next. This evolution of importance for different powers can be demonstrated by observing how the most valuable sector in the economy has changed over time, along with the relevant Power that gave each sector their dominance:

- The major oil companies had cornered resources in the 1980s

- The banks had scale economies in the 1990s

- The internet saw the rise of network economies in the 2000s

- Cloud/SaaS relied on switching costs from the 2010s

In the GenAI era, the ranking of Powers is likely to be reshuffled again. We’ve already discussed how the importance of scale economies in software will likely be reduced due to advances in AI coding. We believe network economies and switching costs will continue to be relevant, but they will increasingly be driven by data (e.g. through personalisation or fine-tuning models based on learnings across customers). There may even be a new Power we haven’t yet considered, but this is hard to predict.

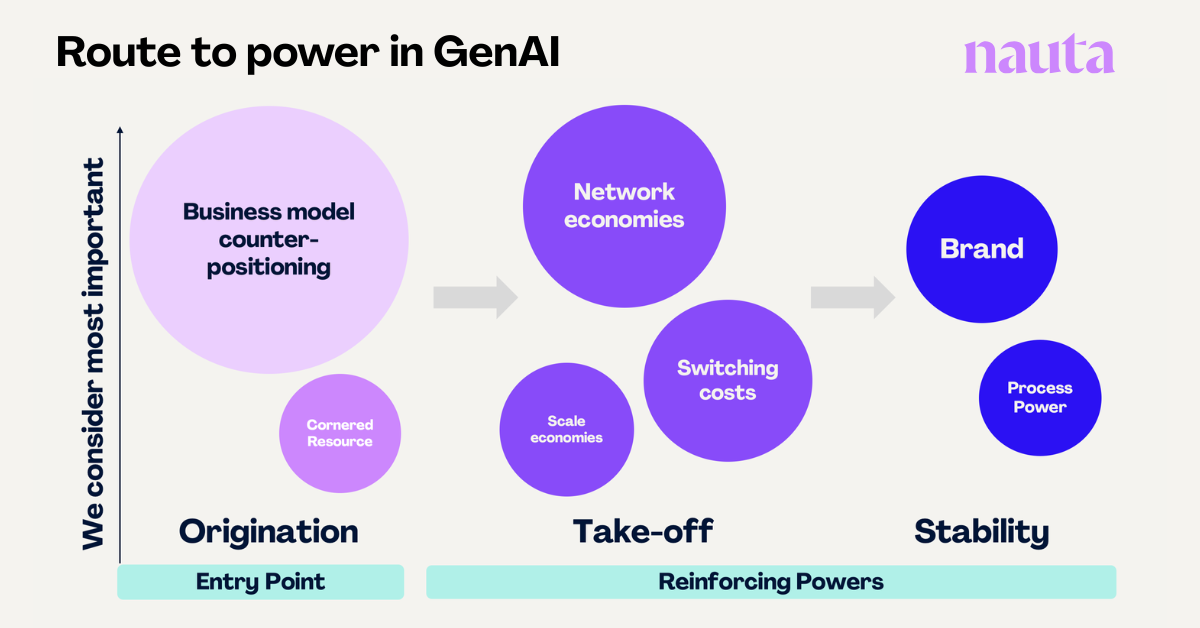

What are the potential sources of Power in the GenAI era?

The companies we are most excited about begin with a counter-position that an incumbent can’t easily copy without harming their existing business.

This might be:

- An existing (or possibly new) workflow with a new AI-native UX/UI

- An entirely new business model (e.g. AI law firms/recruiters at a lower cost than traditional firms could replicate).

Incumbents, even digital natives, are racing to embed AI into their products. They have the advantage of distribution and proprietary data, but they’re constrained by legacy product design and workflows. This opens the door for disruption.

However, to compete with other AI-native companies, you need a route to another Power. We show possible sources below.

Assessing defensibility at the early stage

As different powers are only accessible at different life stages, as early-stage investors, we should look for companies with:

- A product that has value beyond the API (i.e. integrations, thoughtful architecture, improves with underlying models, appropriate handling of non-determinism, solves a real problem for customers)

- One, or both, of the origination powers: counter positioned business model and/or cornered resource(although the latter is much rarer in software)

- A route to one of the other powers (switching costs, network economies, brand, scale economies, process power)

- Executional, product and commercial excellence are necessities but NOT powers*

- The right timing: Strong ‘why now?’ for what they are building. Have founding insight to create or shape a category

The difficult route to Power for horizontal technologies

While we challenge the idea that momentum alone is enough, we do acknowledge, as Helmer notes, “early relative scaling is critical for Power. Who scales the fastest is often determined by who gets the product most right early on.”

In horizontal plays, we’ve seen this play out in Europe with early AI leaders like Synthesia, Eleven Labs and Lovable. Finding a counter-position, building the ‘right’ product, and investing in community building and strong branding, alongside relentless execution, enabled them to claim the leading position in the categories they are shaping.

But long-term survival for horizontal software will be capital intensive even with strong product-led growth. The more broadly applicable the product, the more vulnerable it is to margin erosion, unless it has an embedded route to Power.

Well-capitalised players like OpenAI, Microsoft, and Google could eventually bundle similar products into their offerings, pressuring price, as we’ve already seen with Anthropic’s Claude Code competing with Cursor. The very reason these products have grown so fast is also what creates doubt around their defensibility. Brand power alone may not be enough.

What makes a vertical GenAI attractive?

At Nauta, capital efficiency has been a pillar of our thesis for a long time - even when the investor community doesn’t favour it. While horizontal products offer massive potential, vertical GenAI companies offer clearer routes to Power.

Would OpenAI compete with a coding assistant or a no-code app builder? Yes.

Against an AI legal copilot? Less likely.

With an AI copilot for logistics or debt recovery? Highly unlikely.

By focusing on specific workflows and customer needs, these companies are better positioned to:

- Deliver differentiated experiences

- Layer intelligence over existing systems of record

- Redefine how industries operate

We’re especially keen on verticals with vast amounts of unstructured data and manual processes that are ripe for digital transformation. Sectors like legal services, travel, and manufacturing offer enormous potential for insurgent software providers, as incumbents are slower moving.

Below are some of the verticals where several GenAI companies are already showing defensibility thanks to their solutions embedding deeply into workflows, leveraging domain-specific data, and solving high-stakes problems that incumbents struggle to address.

- Legal - While Harvey and Legora have scaled rapidly by serving lawyers directly, we’re excited by emerging niches like jurisdiction-specific (Lexroom in Italy) and specialism-specific tooling (Wexler in litigation strategy). Beyond tooling, we see structural shifts underway: AI-native firms (Crosby, Eve, Lawhive) counter-positioning against legacy providers, billing innovation (Narrative, Ayora), and in-house enablement tools that help legal teams triage, draft, and negotiate internally.

- Compliance & certification - Platforms like Secfix and Complaion automate certification and audit processes, offer real-time monitoring, and integrate deeply with systems of record. By building jurisdiction-specific workflows and auditor networks, these European challengers create defensible moats against US incumbents like Vanta.

- Financial services & insurance - The opportunity to automate high-stakes workflows across decisioning and compliance (Rekord, Covecta, Umony), and customer support (Gradient Labs). These tools offer deep integrations with legacy systems and explainable decisioning - essential for building trust in regulated, data-rich environments.

Founders need deep domain knowledge to build truly defensible GenAI companies. While the initial market size may be small, proving you have both a right to shape a category in that niche and a credible wedge into a broader one is key.

What’s next?

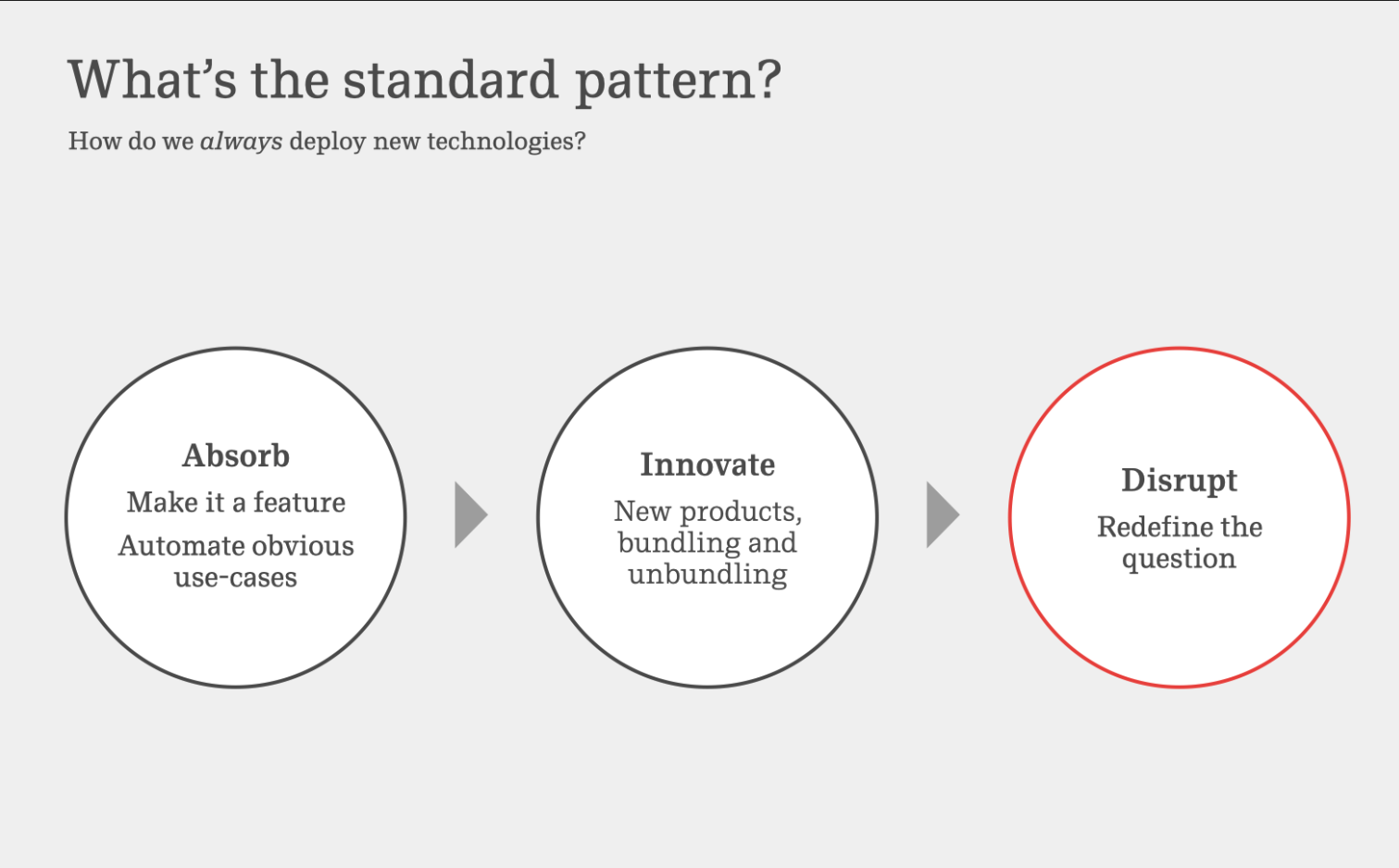

There’s already a lot of FOMO in the GenAI market, but we should remember that we’re still in the early phases of a major platform shift. Of the three phases Benedict Evans outlines for the deployment of new technologies, we’re largely still in Phase 1.

Source: Benedict Evans, ‘AI Eats the World’

The companies that will define this GenAI era might look different. More like “huge… if it works” than “seems to be working, let’s hope it scales.” As investors, we must stay open-minded while we are seeking alpha.

In summary, momentum matters, but don’t neglect your route to Power. Execution excellence is a necessary condition to scale, but long-term durability requires a thoughtful approach to defensibility from the start.

If you're building something that redefines ways of working in an industry, or if you're thinking deeply about defensibility as you build your company, we want to hear from you.