What do junior VCs need to know about term sheets?

Last week, we hosted the second Fundamentals workshop for junior VCs, focused on term sheets. The session was led by Jean de Fougerolles (Managing Partner at Ascension) and marked the second event in a series I'm running alongside Freya Wordsworth (Associate at Ascension).

What is Fundamentals?

Fundamentals is a series of educational sessions created by junior VCs, for junior VCs. We’re fortunate at both Nauta and Ascension to receive great training, but even with that, a lot of learning happens on the job. This session was mostly focused on the VC perspective and for startup founders looking to learn the basics of terms sheets, we’d recommend reading SeedLegal’s introduction.

As there is no ‘VC textbook’, we wanted to create the resources we wish we had to learn from and create a space to learn from experienced investors. In doing so, we hope this better equips us to make the investment process as smooth as possible for startups. You can read about the first session here.

Term Sheet Basics

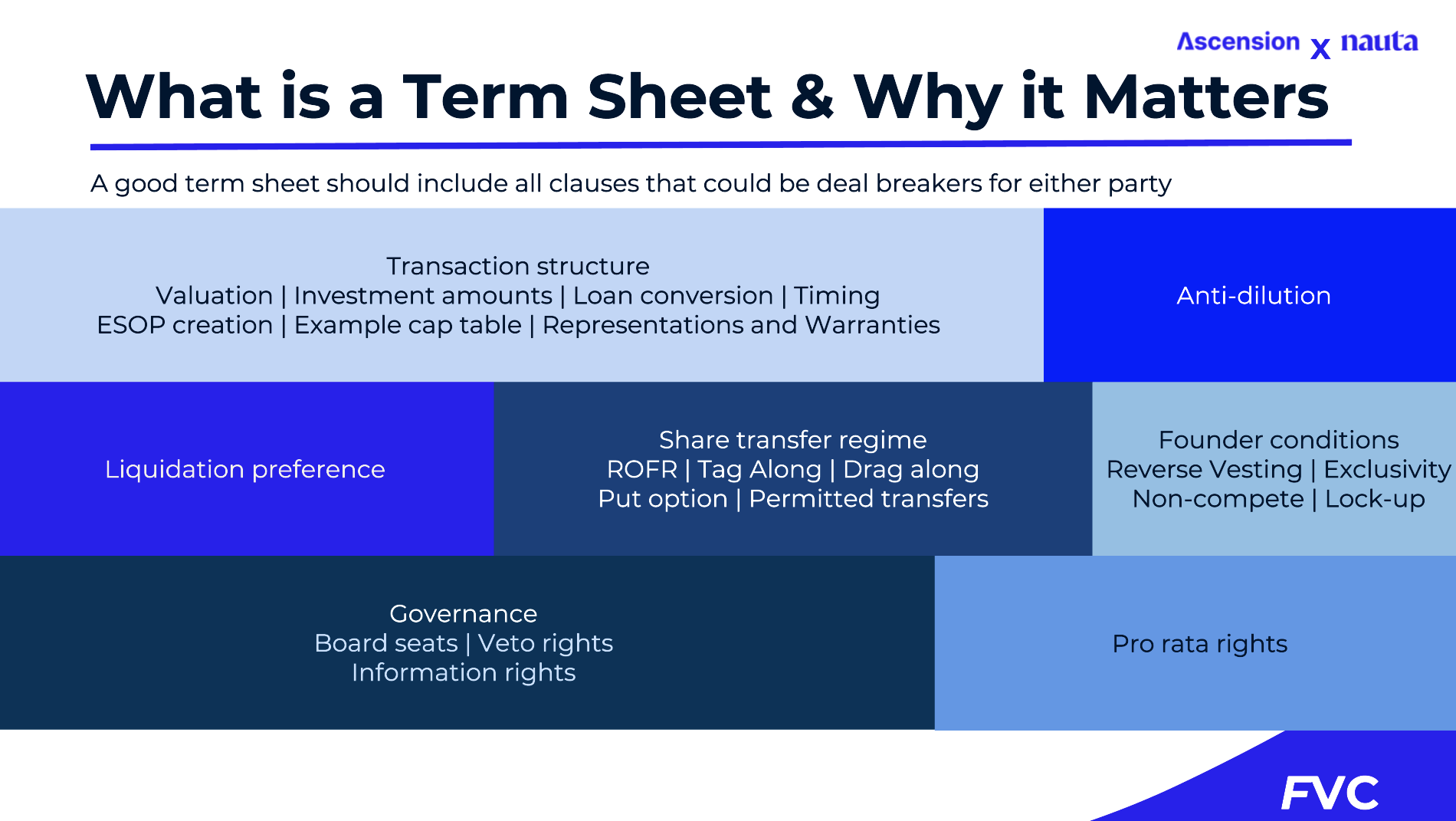

A term sheet is more than a summary of deal terms; it’s the first formal step in the founder-investor relationship. Whilst the terms are non-binding, the document sets the tone and expectations for what could become a long-term partnership and should cover most of the potential dealbreakers for both founders and investors. Having alignment early avoids surprises later, reduces legal costs for both parties, and builds trust.

Whilst each fund has different preferences and non-negotiables, there are certain core principles that are key to protecting both founders' and investors' rights.

Beyond the transaction structure (e.g. amount invested, pre-money valuation), a term sheet will typically also layout key clauses and rights for the investor(s) (e.g. governance rights, founder conditions, share transfer rules and investor protections).

Key Clauses

In the session, we walked through the core clauses typically found in a term sheet - not just what they are, but why they exist. Jean shared real-world examples from his experience to illustrate the important principles behind each clause and how they can protect both investors and founders.

Investor consent rights: These rights are safeguards for all shareholders. They are designed to ensure that investors, who are contributing significant capital, have oversight over decisions that could materially affect the value or direction of the company. Such major decisions could include issuing new shares, raising a new funding round, hiring key personnel and selling the company.

For example, at the early stages, the founders own the majority of the shares and so would control the board. Therefore, without consent rights, a founder could theoretically approve a £2M salary for themselves or sell the company for far less than its worth.

Reverse vesting: Reverse vesting means founder shares are earned over time (typically over four years) and is one of the most frequently questioned clauses in a term sheet. It can feel counterintuitive to founders, especially those who’ve already invested significant time and effort into building the company. But as Jean highlighted in the session, it’s not about penalising founders. It’s about protecting the company and the team that remains if someone steps away.

Early-stage investors are backing the founders as much as the business. Without reverse vesting, a founder could technically walk away with a large equity stake shortly after funding. This clause ensures equity stays with those actively building the company and allows unvested shares to be reallocated if someone leaves. This protects the remaining team members and ensures future hires can be incentivised.

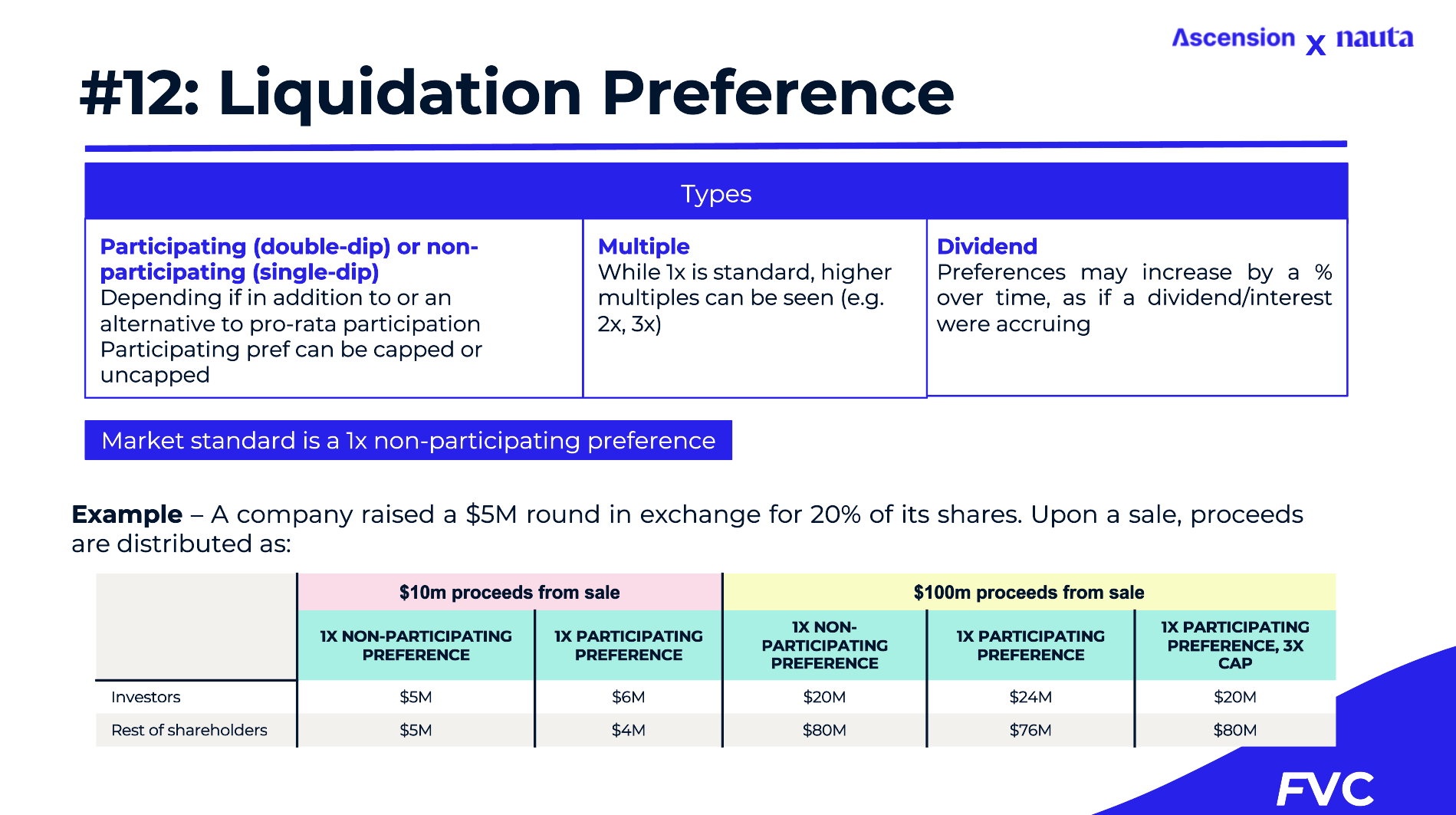

Liquidation preferences: This clause determines who gets paid first if the company is sold. It protects investor downside without limiting founder upside in strong exits. It is something founders should understand clearly as it can impact their ultimate outcome. The market standard is a 1x non-participating preference (opposed to a participating preference or a multiple >1x).

Final Thoughts

While most term sheet clauses are non-binding, there’s a strong reputational expectation that both sides will honour what’s agreed. Founders and investors rely on mutual trust and market norms to carry the deal forward smoothly. By approaching term sheets with clarity and empathy, junior VCs can help make the process more constructive for everyone involved.

While this session focused on term sheets from a VC perspective, it’s equally important to consider how these clauses land with founders. Terms like reverse vesting or liquidation preferences can feel unfamiliar at first, but when explained clearly and structured fairly, they help build alignment and trust.

For founders looking to explore these topics further, platforms like SeedLegals and CooleyGO offer accessible breakdowns of market standards and legal terms. I also found the chapter on term sheets in the book Founder vs Investor, by Elizabeth Zalman & Jerry Neumann, particularly insightful. It’s a great resource for understanding both sides of the table.

Thank you for reading!

If you have any questions about term sheets and the materials referenced here, please contact me (ana.fernandez@nautacapital.com) or Freya (freya@ascension.vc). Equally, if you would like to attend a future Fundamentals event or have requests for topics we should cover, we’d love to hear from you.